Fraud Red Flags

Fraud Definition

Reasons Fraud Is Committed

Impact of Fraud

Fraud Prevention

Fraud Detection

Reporting and Investigating Fraud

Identifying Fraud Red Flags

Definition of Fraud TOP

Fraud may be defined as an intentional act or omission designed to deceive others, resulting in the victim suffering a loss and or the perpetrator achieving a gain. According to the Association of Certified Fraud Examiners, the typical organization loses 5% of its annual income to fraud. www.acfe.com

Fraud encompasses an array of irregularities and illegal acts characterized by intentional deception. The elements of fraud are:

- A representation about a material fact

- Which is false

- And made intentionally, knowingly, or recklessly

- Which is believed

- And acted upon by the victim

- To the victim's damage

Why do people commit Fraud? TOP

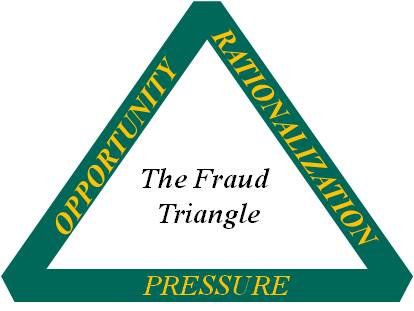

Employees who commit fraud generally are able to do so because there is opportunity, pressure and rationalization. The phases of fraud are best illustrated by The Fraud Triangle below.

Opportunity is generally provided through weaknesses in the internal controls such as inadequate or lack of:

- Supervision and review

- Separation of duties

- Management approval

- System controls

Pressure can be imposed due to:

- Personal financial problems

- Personal vices such as gambling, drugs, extensive debt, etc.

- Unrealistic deadlines and performance goals

Rationalization occurs when the individual develops a justification for their fraudulent activities. The rationalization varies by case and individual. Some examples include:

- "I really need this money and I'll put it back when I get my paycheck"

- "I'd rather have the company on my back than the IRS"

- "I just can't afford to lose everything "" my home, car, everything"

TOP

How does fraud impact the University?

Fraud hurts everyone. Fraud is a common risk that should not be ignored. Failure to do so will eventually result in damaging morale, jeopardizing the reputation of the university and raise questions about its fiduciary duties regarding funds provided by donors, government agencies, students, and parents. Fraud costs everyone through direct influence or indirectly through increased taxes and costs of products and services.

Common fraud schemes which occur at universities include the misuse of procurement cards ("p-cards"), padding expense accounts, listing fictitious vendors, rigging vendor bids, taking kickback and abusing payroll and overtime by fraudulent reporting of hours worked.

TOP

Fraud Deterrence and Prevention

The key deterrent of fraud is awareness and prevention. Processes which are deemed most effective for fraud prevention are denial of opportunity, effective leadership, auditing and employee screening. Denial of opportunity may be translated in the form of internal controls and consistently adhering to clearly defined University procedures established by leadership.

Internal Audit's strategy to examining the effectiveness of internal controls, policies and procedures leadership has established consist of annual fraud risk assessments are performed and periodically revisit them; implementing fraud prevention and detection strategies; developing response strategies for the frauds they aren't able to prevent.

TOP

Who is responsible for detecting fraud?

Fraud should be detected by personnel in the normal course of performing their duties, if strong controls exist. Internal auditors should have sufficient knowledge of fraud to ensure that they may identify indicators that fraud might have been committed. If significant control weaknesses are detected, additional tests conducted by internal auditors should include tests directed toward identification of other indicators of fraud. Internal auditors are not expected to have knowledge equivalent to that of a person whose primary responsibility is to detect and investigate fraud. Audit procedures alone, even when carried out with due professional care, do not guarantee that fraud will be detected.

The Office of Internal Audit is developing a fraud Awareness Program designed to increase your level of fraud awareness as it relates to your roles and responsibilities here at Wayne State University.

TOP

Reporting Fraud

Fraud is a common risk that should not be ignored. All employees have an obligation to report any suspicions or allegations of fraud. to protect the reputation and integrity of the University. Strong fraud prevention processes help increase the confidence students,donors, regulators, board members and the general public have in the integrity of our University and its ability to manage its fiduciary responsibilities.

Fraud Awareness Education is the foundation of preventing and detecting occupational fraud, within the Schools, Colleges and Divisions of Wayne State University. Students, Faculty and Staff members must be educated in what constitutes fraud, how it hurts everyone at WSU and how to report any questionable activity.

Who should I call about an alleged fraud?

If you suspect fraud, any suspicious activity misuse, misappropriation, etc., please contact the Office of Internal Audit at the Fraud Hotline 313-577-5138. For Online Reporting submit an Anonymous Tips Form. If the fraud involves stolen or misappropriated assets (e.g., cash, property, equipment, etc.), you should also call Public Safety at 7-2222 to file an incident report.

What will happen if I report an alleged fraud?

All information related to the specific situation is confidential. Employees are not singled out as "whistle-blowers", however, management is notified of the particular situation in order that a full investigation may be conducted.

How is a fraud investigation conducted?

Fraud investigations may be conducted by or involve the participation of the Office of Internal Audit, Public Safety, General Counsel, C&IT Security, and other areas of the University as appropriate. The Office of Internal Audit will assess the facts known relative to all fraud investigations in order to:

- Determine the need to implement or strengthen controls

- Design audit tests to identify similar frauds in the future

The Office of Internal Audit may:

- Conduct inquiries to obtain an understanding of the situation

- Review supporting documentation

- Request or confirm information with outside parties such as banks

- Review departmental and university policies and procedures

- Make recommendations to management to change areas of noncompliance or strengthen controls

- Contact Public Safety if a crime has been committed

TOP

Identifying the "Red Flags" of fraud

Red Flags within an organization are related to the structure of the organization and the manner in which its policies and procedures are implemented. Understanding symptoms of fraud is the key to detecting fraud. A symptom of fraud may be defined as a condition which is directly attributable to dishonest or fraudulent activity. It may result from the fraud itself or from the attempt to conceal the fraud.

Factors contributing to fraud: TOP

- Lax or ineffective internal controls

- Ineffective management

- Management or control overrides

- Collusion among employees over whom there is little to no supervision

- Lack of account review reconciliation

- When significant policies are absent or outdated (e.g.,code of ethics,transparency, periodic monitoring of business and academic performance indicators,management systems,internal audit procedures and annual external financial audits)

- The presence of unethical behavior poses significant risk to any organization

Embezzlement "Red Flags" TOP

- Borrowing money from co-workers

- Creditors or collectors appearing at the workplace

- Gambling beyond the ability to stand the loss

- Excessive drinking or other personal habits

- Easily annoyed at reasonable questioning

- Providing unreasonable responses to questions

- Refusing vacations or promotions for fear of detection

- Bragging about significant new purchases

- Carrying unusually large sums of money

- Rewriting records under the guise of neatness in presentation

Common Forms of Fraud in Higher Education TOP

- Personal purchases on the procurement card

- Inappropriate charges to a travel or account payable voucher

- Theft of inventory items

- Theft of cash from deposits

- Falsifying time card with time not worked

- Misappropriation of Assets

- Compliance

- Conflict of Interest

- Unauthorized System Changes

- Forgery

- Identity Theft

- Kickbacks

- Bribery

- Misrepresentation/Concealment of material facts

- Theft of money or property

- Theft of trade secrets or intellectual property

- Breach of fiduciary duty

- Rumors of conflicts of interest

- Using duplicate invoices to pay vendors

- Frequent use of sole-source procurement contracts

- No supporting documentation for adjusting entries

- Incomplete or untimely bank reconciliations

- Increased customer complaints

- Write-offs of inventory or cash shortages with no attempt to determine the cause

Danger Signs of Fraud TOP

- High personnel turnover

- Low employee morale

- No supporting documentation for adjusting entries

- Incomplete or untimely bank reconciliations

- Increased customer complaints

- Write-offs of inventory shortages with no attempt to determine the cause

- Unrealistic performance expectations

- Rumors of conflicts of interest

- Using duplicate invoices to pay vendors

- Frequent use of sole-source procurement contracts

- Unreconciled accounts

- Dormant accounts

- Failure to deactivate or terminate access after employees have separated from a position, unit or the university